Mine closure costs have a habit of arriving late in the conversation.

They are often discussed late, challenged late and corrected late. By the time the true cost of closure is properly understood, the mine plan, asset valuation, rehabilitation strategy, accounting provision and public commitments may already have been built around a number that was too narrow, too optimistic or prepared for a different purpose altogether.

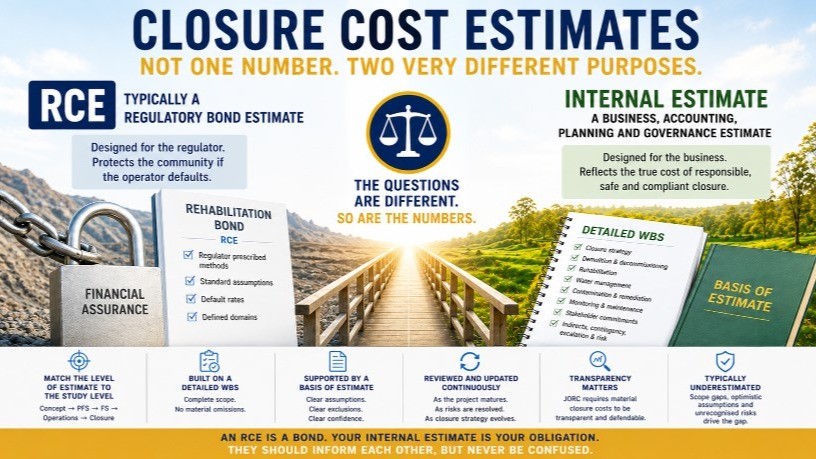

At the centre of the issue is a common misunderstanding: the assumption that a Rehabilitation Cost Estimate (RCE) is the same as an internal closure cost estimate.

It is not – in fact, they are fundamentally different tools.

“Too often, the Rehabilitation Cost Estimate is treated as the mine’s closure cost. It is not. An RCE is typically a regulatory bond estimate. The internal provision must be a properly scoped, study-aligned estimate built from a detailed WBS and supported by a clear Basis of Estimate. If closure costs are material to the business, they need to be estimated, reviewed and governed with the same discipline as the rest of the project. Otherwise, we risk mistaking a compliance number for the real cost of responsible closure.”

The RCE is typically a bond estimate

A Rehabilitation Cost Estimate is typically prepared to support a rehabilitation bond, security deposit or financial assurance requirement.

Its primary purpose is regulatory.

The RCE is generally intended to estimate the cost that may be required for a regulator or government to step in and complete rehabilitation works if the operator defaults. It is often prepared using regulator-prescribed methods, standardised assumptions, default rates, template structures and defined rehabilitation domains.

For that purpose, it has value.

But that does not make it a complete internal closure estimate.

An RCE is not usually designed to reflect the company’s preferred closure strategy, commercial execution model, accounting provision, life-of-mine planning assumptions or full residual liability position.

It may not fully capture the way the company actually intends to close the asset.

It may not reflect internal delivery efficiencies, staging, procurement strategy, owner’s costs, indirect costs, post-closure risk management or the full range of closure obligations that sit outside the bond calculation.

Yet we still coming across site accountants and managers who rely on the RCE as the internal closure estimate.

It simply is not.

An RCE is typically a regulatory bond estimate.

An internal closure estimate is a business, accounting, planning and governance estimate.

They may inform each other, but they should never be treated as interchangeable.

Why the distinction matters

Using an RCE as the internal closure cost estimate can materially understate the true closure liability.

That has consequences across the business. It can affect asset valuation, life-of-mine planning, Ore Reserve economics, accounting provisions, transaction due diligence, capital allocation, board reporting, investor confidence and closure readiness.

A bond estimate is usually designed around a regulator’s security framework.

An internal estimate should be designed around the company’s actual closure obligation.

Those are not the same question.

The RCE asks, in effect:

What amount of security should be held to protect the regulator and the community if the operator defaults?

The internal estimate should ask:

What will it actually cost us to close this asset responsibly, safely, lawfully and in accordance with our commitments?

Those two questions can produce very different answers.

A proper internal provision needs structure

An internal closure provision should not be a copied RCE, a high-level benchmark or a single line item in a financial model.

It should be assessed against a detailed Work Breakdown Structure, or WBS, that reflects the actual scope of closure.

That WBS should break closure into logical, auditable and costable packages, including planning, approvals and studies; progressive rehabilitation; final landform construction; demolition and decommissioning; asset recovery and salvage; hazardous materials and waste management; contamination assessment and remediation; water management and treatment; mine sealing and geotechnical controls; infrastructure removal; access tracks, drainage and erosion controls; monitoring and maintenance; stakeholder engagement and reporting; owner’s costs, project management and indirect costs; and contingency, escalation and residual risk allowances.

The estimate should also be supported by a clear Basis of Estimate.

That Basis of Estimate should explain what the estimate is based on, what is included, what is excluded, what assumptions have been made, what quantities and rates have been used, what level of engineering definition supports the estimate, what risks remain unresolved, and what level of accuracy is being claimed.

Without a WBS and a Basis of Estimate, it is very difficult for management, auditors, boards or investors to understand whether the provision is complete, reasonable or aligned with the actual closure obligation.

The estimate must mature with the study

Closure cost estimates should mature as the project matures.

A conceptual closure strategy should not carry the same estimating confidence as a detailed closure execution plan. Equally, a feasibility-level mine plan should not rely on a closure estimate that remains at a broad benchmarking level.

As projects move from concept, pre-feasibility, feasibility, operations, late-life planning and execution, the closure estimate should also move through increasing levels of definition.

That means improving scope definition, domain-based quantities, demolition and decommissioning assumptions, rehabilitation methods, material balances, water management and water treatment assumptions, contamination liabilities, mine sealing and residual geotechnical risks, final landform drainage performance, long-term monitoring and maintenance requirements, post-closure obligations, contractor rates, productivity and indirect costs, owner’s costs, contingency and escalation assumptions.

The estimate should be continually reviewed and updated so that its level of accuracy matches the relevant study protocol.

A PFS-level closure estimate should have the scope definition, contingency, risk allowance and accuracy range expected for a PFS.

An FS-level closure estimate should have the engineering definition, quantity confidence, procurement assumptions, schedule logic and cost accuracy expected for an FS.

Closure should not sit outside the study process.

It should be estimated with the same discipline as the mining, processing, infrastructure and sustaining capital components of the project.

The level of estimate should be clear. The confidence range should be clear. The exclusions should be clear.

A single closure number without context is not enough.

JORC is lifting the bar

Closure costs are also becoming more important in public reporting.

The JORC Code is built around the principles of transparency, materiality and competence. Where closure costs, environmental obligations, rehabilitation commitments or post-mining liabilities are material to the economics of a project, they need to be properly considered and transparently explained.

That matters because closure is no longer a peripheral issue.

Closure can materially affect Ore Reserve economics, project value, residual liability, financing and transaction due diligence, social licence, regulatory approval pathways, board confidence and investor confidence.

If closure assumptions are material to the economics of a project, they need to be capable of being defended.

Why closure costs are so often underestimated

In practice, closure costs are often underestimated because the early estimate is too narrow, too generic or based on the wrong estimating framework.

The issue is not always the unit rate.

Often, the issue is the scope.

Common omissions include demolition and decommissioning complexity, hazardous materials and waste classification, contaminated land investigation and remediation, water treatment beyond mining, long-term monitoring and maintenance, mine sealing and subsidence risks, final landform drainage performance, approvals, consultation and specialist studies, indirect costs, owner’s costs and contractor margins, schedule risk and escalation, and residual risks that remain after rehabilitation is complete.

A low closure estimate can look attractive in the short term.

But it can distort asset value, understate liabilities, misinform investment decisions and leave management teams with a funding gap later in the mine life.

A robust closure provision helps boards, executives, technical teams and investors understand the real cost of responsible closure and the value of making better closure decisions earlier.

Closure is not just an environmental obligation.

It is a material business issue.

And an RCE should never be mistaken for the full internal cost of closure.